Property Tax Deduction: Homeowners can deduct the amount they pay in property taxes on their primary residence and any other real estate they own. The property tax deduction is an itemized deduction and can help reduce your taxable income.

What’s Ahead For Mortgage Rates This Week – November 13, 2023

The week following the FOMC rate decision meetings are typically very light, with the two most influential releases being the University of Michigan Consumer Sentiment and the weekly Job Claims reports. The more positive news is mortgage lending rates have been on the decline in the last two weeks.

How to Go From Renting to Owning a Home

Going from renting to owning a home can be a significant financial and personal milestone, but it requires careful planning and preparation. Here are some steps to take to make the transition from renting to owning:

Going from renting to owning a home can be a significant financial and personal milestone, but it requires careful planning and preparation. Here are some steps to take to make the transition from renting to owning:

Determine your budget: Calculate your current expenses and income to determine how much you can afford to spend on a home. Consider factors such as down payment, closing costs, monthly mortgage payments, property taxes, and homeowner’s insurance.

Save for a down payment: A down payment is typically required when purchasing a home, and the larger the down payment, the lower your monthly mortgage payments will be. Aim to save at least 20% of the home’s purchase price to avoid paying private mortgage insurance (PMI).

Mortgage Rate Locks: When and How to Secure a Favorable Rate

Securing a mortgage to purchase your dream home is a significant financial decision. One of the essential aspects of this process is locking in a favorable mortgage rate. A mortgage rate lock ensures that the interest rate on your loan remains the same for a specified period, protecting you from potential rate fluctuations. We will explore when it’s best to lock in a mortgage rate and provide a step-by-step guide on how to do it.

Securing a mortgage to purchase your dream home is a significant financial decision. One of the essential aspects of this process is locking in a favorable mortgage rate. A mortgage rate lock ensures that the interest rate on your loan remains the same for a specified period, protecting you from potential rate fluctuations. We will explore when it’s best to lock in a mortgage rate and provide a step-by-step guide on how to do it.

When to Lock in Your Mortgage Rate

The perfect time to lock in your mortgage rate depends on various factors, and it’s not an exact science. Here are some key considerations to keep in mind:

Understanding Assumable Mortgage Loans

Mortgage loans are an essential aspect of financing the purchase of a property. Among the various types of mortgages available, one option that may be advantageous for both buyers and sellers is an assumable mortgage loan.

Mortgage loans are an essential aspect of financing the purchase of a property. Among the various types of mortgages available, one option that may be advantageous for both buyers and sellers is an assumable mortgage loan.

An assumable mortgage loan is a type of home loan agreement that allows a homebuyer to assume the existing mortgage of the seller when purchasing a property. In other words, the buyer takes over the seller’s mortgage terms and conditions, including the interest rate, repayment schedule, and remaining balance.

The Role of A Down Payment: How Much Should I Save?

Buying a home, a car, or any significant investment often involves making a down payment. The down payment is a crucial part of the purchasing process, as it can impact your loan terms, interest rates, and monthly payments. But how much should you save for a down payment, and why is it so important?

Buying a home, a car, or any significant investment often involves making a down payment. The down payment is a crucial part of the purchasing process, as it can impact your loan terms, interest rates, and monthly payments. But how much should you save for a down payment, and why is it so important?

Understanding Down Payments

A down payment is a portion of the purchase price that you pay upfront when buying a house, a car, or making a large investment. It’s a way to demonstrate your commitment to the purchase and reduce the risk for the lender or seller. Down payments are commonly associated with:

What’s Ahead For Mortgage Rates This Week – November 6, 2023

The most important data of the quarter was released, signaling the direction for many markets and where economic policy may be headed. Jerome Powell as well as other members of the Federal Reserve spoke about the state of economic policy, informing many parties about their decisions to remain hawkish or dovish in their approach. Further rate hikes could tell a story that inflation is not yet under control and the Federal Reserve feels the need to continue these rate hikes, which will have a significant impact on the lending markets as a whole.

The most important data of the quarter was released, signaling the direction for many markets and where economic policy may be headed. Jerome Powell as well as other members of the Federal Reserve spoke about the state of economic policy, informing many parties about their decisions to remain hawkish or dovish in their approach. Further rate hikes could tell a story that inflation is not yet under control and the Federal Reserve feels the need to continue these rate hikes, which will have a significant impact on the lending markets as a whole.

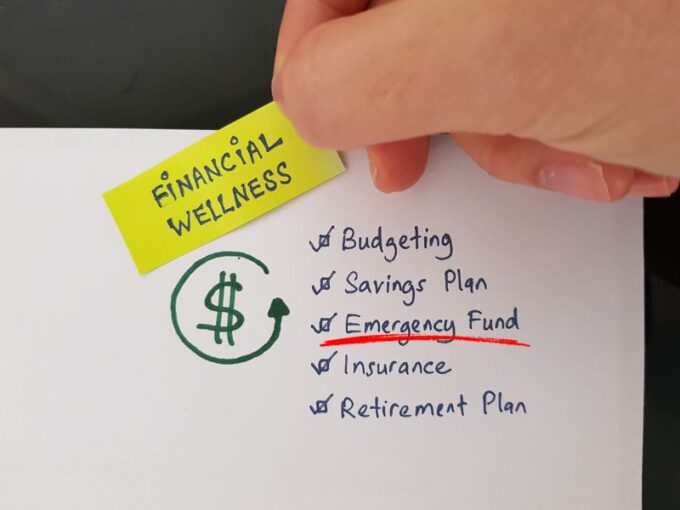

Ways To Be Financially Prepared for an Emergency

It’s important to be financially prepared for emergencies so that you can handle unexpected expenses or situations without having to worry about your financial stability. Here are some ways to financially prepare for emergencies:

It’s important to be financially prepared for emergencies so that you can handle unexpected expenses or situations without having to worry about your financial stability. Here are some ways to financially prepare for emergencies:

Build an emergency fund: Start by building an emergency fund that can cover at least 3-6 months of your living expenses. This fund should be kept in a separate savings account and should only be used for emergencies.

Create a budget: Create a budget and stick to it. This will help you identify areas where you can cut back on expenses and save more money.

Will Getting a Mortgage Help My Credit Score?

Getting a mortgage can potentially help your credit score, as long as you make your payments on time and in full each month. Payment history is one of the most important factors that influence your credit score, so consistently making your mortgage payments on time can have a positive impact on your credit score over time.

Getting a mortgage can potentially help your credit score, as long as you make your payments on time and in full each month. Payment history is one of the most important factors that influence your credit score, so consistently making your mortgage payments on time can have a positive impact on your credit score over time.

It is important to carefully consider the financial implications of taking on a mortgage and to ensure that you can afford the payments before proceeding. It is also important to keep in mind that taking out a mortgage will also result in a hard inquiry on your credit report, which can temporarily lower your credit score.

Planning Your Mortgage Budget for the Holiday Season

The holiday season is a time of joy and celebration, but it can also be a challenging time for your finances, especially if you’re juggling the responsibilities of a mortgage. However, with some thoughtful planning and budgeting, you can ensure that you enjoy the festivities without putting your financial stability at risk. I will provide you with essential tips and strategies to help you manage your mortgage budget during the holiday season.

The holiday season is a time of joy and celebration, but it can also be a challenging time for your finances, especially if you’re juggling the responsibilities of a mortgage. However, with some thoughtful planning and budgeting, you can ensure that you enjoy the festivities without putting your financial stability at risk. I will provide you with essential tips and strategies to help you manage your mortgage budget during the holiday season.

Create a Holiday Budget

Set a specific budget for your holiday expenses. This budget should encompass everything from gifts and decorations to travel and entertainment. By creating a clear budget, you can ensure that you don’t overspend, keeping your mortgage payments on track.

- « Previous Page

- 1

- …

- 23

- 24

- 25

- 26

- 27

- …

- 292

- Next Page »